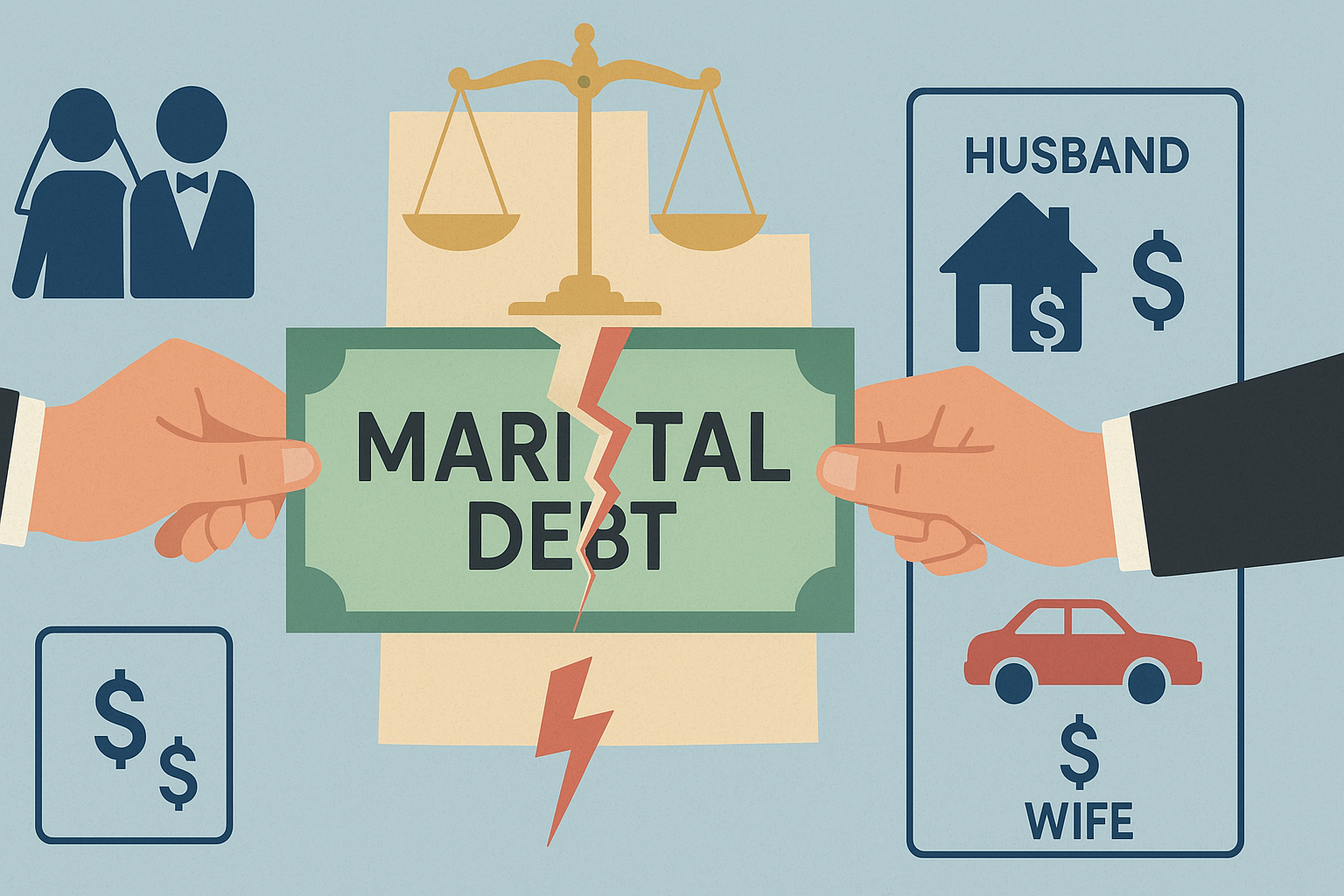

Marital debt division is one of the most important and most confusing parts of a Utah divorce. While many people focus on homes, cars, or retirement accounts, how the court divides credit cards, loans, and other debts can shape each spouse’s financial future for years.

Utah follows an equitable distribution system, which means debts are divided fairly, not always equally. Gibb Law Firm helps Utah clients understand how judges look at marital versus separate debt, what “fair” means in practice, and how to protect themselves when negotiating a divorce settlement or going to court.

Why Marital Debt Division Matters in Utah

Debt does not simply “stay with” the person whose name is on the account. In Utah, the court looks at when and why the debt was incurred, and whether it benefited the marriage. A careful approach can prevent one spouse from being unfairly saddled with more than their share or from being surprised by creditors later.

Marital debts are often shared responsibilities, even if only one spouse’s name appears on a credit card or loan agreement.

Poorly structured debt division can lead to long-term financial strain, credit damage, and enforcement disputes after the divorce.

A fair debt plan should account for current balances, interest rates, and each spouse’s ability to pay once they are living separately.

Clear court orders and written agreements reduce the risk that one spouse stops paying, leaving the other exposed to collection efforts.

The following video gives a helpful overview of how Utah courts think about dividing both assets and debts in a divorce.

Watch: Division of Assets and Debts in Utah

How Utah Courts Classify and Divide Marital Debt

Before the court can decide who pays what, it first classifies each debt. The judge will consider whether the debt is marital or separate, secured or unsecured, and whether it primarily benefited one spouse or the family as a whole.

Marital vs. Separate Debts

Debts incurred during the marriage for household or family purposes are usually treated as marital, even if only one spouse signed for them. Debts from before the marriage or for clearly personal reasons may be treated as separate.

Secured vs. Unsecured Debts

Mortgages and car loans are tied to specific property, while credit cards and personal loans are unsecured. Courts often pair secured debts with the asset (for example, awarding a car and the car loan together).

Joint Accounts and Individual Accounts

A credit card in one spouse’s name can still be a marital debt if it paid for groceries, medical expenses, or family travel. Utah courts look at the purpose of the debt, not just whose name is on the bill.

Because so many moving parts are involved, the “math” of debt division can feel overwhelming. This short reel offers a relatable look at how assets and debts land on each side of the ledger during divorce.

This “Divorce Math?!” explainer highlights why both assets and debts must be considered together when negotiating a fair Utah divorce settlement.

Key Definitions and Utah Statutes

Utah law gives courts wide discretion to divide marital property and debts equitably. Understanding a few core terms can make the process easier to follow.

Marital Debt: Obligations incurred during the marriage for the benefit of the family or household, such as mortgages, car loans, and family credit card balances.

Separate Debt: Debt that is clearly tied to one spouse alone often incurred before marriage or for non-marital purposes (for example, a premarital personal loan).

Equitable Distribution: Utah courts divide debts fairly, not always 50/50. Judges may consider income, earning capacity, and which spouse will keep certain assets when deciding who pays what.

Offsets: Courts may award one spouse more property in exchange for taking on more debt, or vice versa, to reach an overall fair outcome.

Utah Code Ann. § 30-3-5: The main statute that authorizes Utah courts to divide property and debts in a divorce, guided by principles of equity and fairness.

The next video takes a deeper look at how Utah judges first classify property and debts before deciding how to distribute them.

Watch: Principles Governing Property Distribution in Utah

Typical Court Procedures for Dividing Marital Debt

While each case is unique, most Utah divorces involving debt follow a similar sequence. Having a roadmap can make the process less intimidating.

Financial Disclosure

Both spouses complete financial declarations listing income, expenses, assets, and every known debt. Supporting documents statements, loan documents, credit reports are usually required.

Classification of Debts

The parties (and eventually the judge, if needed) determine which debts are marital and which are separate, and identify any debts tied to specific property like a home or vehicle.

Negotiation or Mediation

Spouses often work toward a settlement, sometimes in mediation, deciding who will pay which debts and whether any refinancing or payoffs are necessary to protect both sides.

Final Orders and Enforcement

The court enters a decree assigning debts and, if appropriate, linking certain debts to specific assets. If a spouse later fails to pay as ordered, the other may seek enforcement from the court.

Real property and its associated debts mortgages, HELOCs, and liens often require special attention. The following reel illustrates how refinancing and buyouts can work when a home is involved.

This Utah-focused breakdown shows how courts and lawyers address mortgages, equity, and related debts when one spouse wants to keep the house after divorce.

Required Forms and Filings in Utah Debt Division

Debt division is documented through a mix of standard Utah court forms and case-specific agreements. Accuracy and detail are critical, because these documents become enforceable court orders.

Financial Declaration and attachments showing income, expenses, assets, and all known debts with current balances and minimum payments.

Proposed Property and Debt Division or similar schedules listing which spouse will be responsible for each loan, credit card, and other obligation.

Settlement Agreement or Stipulation, where the parties spell out agreed-upon terms for dividing property and debts, often after mediation.

Divorce Decree, which the court signs and enters as the binding order assigning responsibility for each debt between the spouses.

Refinance, assumption, or payoff documentation (outside the court file) when a spouse must remove the other’s name from joint mortgages or loans.

Because creditors are not parties to the divorce, additional steps like refinancing or closing joint accounts may be necessary to fully protect each spouse, even after the decree is entered.

Common Mistakes to Avoid When Dividing Marital Debt

Many people focus on “who gets what” and overlook how debts should be handled. Avoiding a few common missteps can help prevent costly surprises later.

Ignoring debts in one spouse’s name: Assuming you are safe just because you did not sign the loan can be risky. Courts may still treat the obligation as marital if it benefited the family.

Underestimating interest and fees: High-interest credit cards and variable-rate loans can grow quickly. A “small” balance at the time of divorce can become a major burden later.

Relying on verbal promises: “I’ll take care of that debt” is not enough. If it is not in the decree or written agreement, it will be difficult to enforce in court.

Not checking credit reports: Old cards, forgotten loans, and joint accounts often show up on credit reports. These should be identified and addressed before the divorce is finalized.

Assuming the decree changes creditor rights: Creditors are not bound by the divorce decree. If your name stays on a loan, the creditor can still pursue you if payments stop even if your ex was ordered to pay it.

Leaving joint accounts open: Failing to close, refinance, or separate accounts can expose you to new charges and missed payments long after the divorce is over.

When conflict is high and one spouse insists the debt is “not their problem,” clear legal advice becomes especially important. This reel shows how that issue often appears in real life.

This “When Your Ex Says Debt Isn’t Their Problem” explainer underscores why debt terms belong in the decree, not just in side conversations or text messages.

For a more detailed look at how Utah attorneys help structure debt division, the next video focuses specifically on the lawyer’s role in this part of the case.

Watch: How an Attorney Helps Divide Debts in Utah Divorce

Next Steps if You Have Marital Debt in a Utah Divorce

If you are facing a divorce with significant debt, it can help to approach the problem in a structured way. The following steps are a useful starting point before and during your case.

Gather all statements for credit cards, loans, and lines of credit, including account numbers, balances, and interest rates.

Pull a recent credit report to confirm there are no forgotten accounts or joint obligations that need to be addressed in the divorce.

Identify which debts are clearly marital, which appear to be separate, and which are tied to particular assets like a home or vehicle.

Consider whether refinancing, consolidating, or paying off certain debts makes sense as part of the overall settlement strategy.

Talk with a Utah family law attorney about how judges in your district typically handle debt and what a realistic, fair outcome might look like in your case.

Follow through after the decree by closing joint accounts, updating automatic payments, and monitoring your credit to ensure the plan is working as intended.

Gibb Law Firm works with Utah clients to build debt-division plans that are practical, enforceable, and aligned with long-term financial stability, not just what looks fair on paper today.

Understanding Marital Debt Division and Your Rights in Utah

Marital debt division is more than a spreadsheet exercise. It affects where you live, what you can afford, and how quickly you can rebuild after a divorce. Utah’s equitable distribution rules give judges flexibility, but they also make careful preparation and negotiation essential.

By understanding how Utah classifies marital versus separate debt, how courts typically assign responsibility, and what mistakes to avoid, you can better protect your finances and your future. You do not have to navigate that process alone.

For Utah-specific advice and a clear strategy tailored to your situation, Gibb Law Firm offers straightforward, client-centered guidance on property and debt division in divorce.

To learn more or discuss your case with an experienced Utah family law attorney, visit GibbLaw.com/contact to schedule a consultation.

Talk to Gibb Law Firm About Marital Debt Division in Utah

Have questions about who should be responsible for specific debts, how to protect your credit, or what a fair settlement might look like in your divorce? Our team can review your finances, explain your options under Utah law, and help you negotiate or litigate a debt-division plan that works in the real world.

Schedule a Consultation